Two years ago, a client asked me to audit the payment options across fifteen online casinos targeting Australian players. Half of them accepted both PayID and cryptocurrency. Today, after the June 2024 regulatory changes, the landscape looks completely different — and the choice between PayID and crypto is no longer just about speed or convenience. It is a question that touches on legality, banking relationships, and what kind of risk you are willing to carry.

The ban on credit cards and cryptocurrency at licensed Australian gambling operators, which took effect on 11 June 2024, redrew the map. Licensed operators dropped crypto entirely. Offshore casinos — the ones that never held Australian licences to begin with — kept accepting both PayID and Bitcoin, Ethereum, Litecoin, and a growing list of altcoins. That split created a situation where PayID casino vs crypto casino is not a simple feature comparison. It is a choice between two fundamentally different ecosystems with different legal exposures, different protections, and different trade-offs.

What makes this comparison interesting — and what most competitor analyses get wrong — is that the two methods are not really competing for the same player. The person who gravitates toward crypto is usually motivated by privacy, global portability, and the absence of banking intermediaries. The person who prefers PayID values simplicity, Australian-dollar stability, and the safety net of the banking system. Understanding which camp you fall into matters more than any feature-by-feature table.

I am not here to tell you which method is “better.” That depends on what you prioritise. What I can do is lay out the data, explain the regulatory reality, and let you make an informed decision. After eight years of analysing payment infrastructure in Australian iGaming, I have strong views — but I will keep them grounded in facts rather than preferences.

PayID vs Crypto: A Side-by-Side Breakdown

I have run this comparison for clients so many times that the framework is almost muscle memory at this point. Seven criteria matter. Everything else is noise.

Speed

PayID deposits settle in seconds via the NPP — your casino balance updates almost as fast as you can switch apps. Withdrawals, once released by the operator, are equally fast. Cryptocurrency deposits depend on the blockchain: Bitcoin averages ten minutes per confirmation, and most casinos require at least one or two before crediting your balance. Ethereum is faster, typically under a minute for a single confirmation, and stablecoins on layer-2 networks like Tron or Polygon can confirm in seconds. Withdrawals are comparable in speed once the casino broadcasts the transaction.

On pure settlement speed, the methods are close — PayID is faster for deposits because there is no confirmation wait, while crypto can match or beat PayID on withdrawals at the blockchain layer. But the honest truth is that neither method’s settlement speed is the real bottleneck. The casino’s internal processing pipeline — the same KYC checks, AML screens, and batch schedules — applies to both. Whether the operator takes two hours or twelve to approve your withdrawal, that delay is identical regardless of whether the payment goes out via NPP or Bitcoin.

Fees

PayID is free. No transaction fees, no percentage cuts, no gas costs. Crypto carries network fees that vary wildly. A Bitcoin transaction can cost anywhere from A$0.50 to A$30 depending on network congestion. Ethereum gas fees have ranged from under a dollar to over A$100 during peak periods. Stablecoins on layer-2 networks (like USDT on Tron) are cheaper, often under A$1, but introduce additional complexity. For a player making weekly deposits, the fee difference adds up.

Security

PayID transactions are protected by the same banking infrastructure that secures your salary, your rent, and your mortgage payments. The NPP’s confirmation screen shows you who you are paying before you send. Reported PayID-specific scam losses totalled around A$260,000 in 2023 — a rounding error compared to A$854 million in payment card fraud during FY25. Crypto transactions are irreversible and pseudonymous. If you send Bitcoin to the wrong address, it is gone. If the casino’s wallet is compromised, there is no bank to dispute through. Crypto security is strong at the protocol level but weak at the human level — there is no safety net for user error.

Anonymity

PayID links your real name to every transaction. The casino sees your PayID display name, and your bank sees the recipient’s PayID. There is a complete, auditable trail. For regulatory purposes, this is a feature. For personal privacy, it is a constraint — every deposit and withdrawal appears on your bank statement with a clear link to the recipient.

Crypto offers pseudonymity — not full anonymity, as blockchain analysis firms have become very effective at tracing transactions — but significantly more privacy than a bank transfer. Wallet addresses are not inherently tied to a real-world identity unless you used a KYC-verified exchange to acquire the crypto. For players who prioritise keeping their gambling activity separate from their banking records, this is crypto’s single strongest feature. Whether that privacy is worth the trade-offs in protection and convenience is the core question this entire comparison circles around.

Currency and conversion

PayID operates in Australian dollars natively. No conversion, no slippage, no exchange rate risk. Crypto requires converting AUD to a cryptocurrency via an exchange, incurring both the exchange’s fee and any spread between the buy and sell price. When you withdraw, you reverse the process — converting crypto back to AUD — and absorb another round of fees and potential price movement. If Bitcoin drops 5 per cent between your deposit and your withdrawal, your effective cost of using crypto just increased by 5 per cent regardless of whether you won or lost at the casino.

Deposit and withdrawal limits

PayID limits are set by your bank (typically A$1,000 to A$5,000 per day, adjustable) and the casino’s own caps. Crypto has no inherent transaction limit — you can send A$100,000 in Bitcoin in a single transfer if the casino accepts it. This makes crypto the preferred method for high-volume players at offshore sites. PayID’s bank-imposed caps can be restrictive for larger deposits, though most banks will raise the limit on request.

Availability

PayID is available at any casino that accepts Australian bank transfers through the NPP — which includes both licensed and many offshore operators targeting AU players. Its reach is broad because it leverages existing banking infrastructure rather than requiring a separate payment ecosystem. Crypto is available only at offshore casinos, since licensed Australian operators have been prohibited from accepting it since June 2024. This is not a minor distinction. It fundamentally shapes which casinos you can access with each method.

The availability picture is also shifting. As ACMA continues to block offshore casino sites — 1,708 and counting — the pool of accessible crypto-accepting operators shrinks over time. PayID, by contrast, remains available at any operator that maintains an Australian banking relationship, which includes both licensed wagering services and many offshore sites that have not yet been blocked. The long-term trajectory favours PayID’s availability simply because it operates within the financial system rather than outside it.

The Legal Factor: Why It Matters for AU Players

If there is one section of this article you should not skim, it is this one. I have seen too many players treat the legal dimension of payment method choice as background noise — something that applies to operators, not to them. That assumption is mostly correct under current enforcement practice, but “mostly” is doing a lot of heavy lifting.

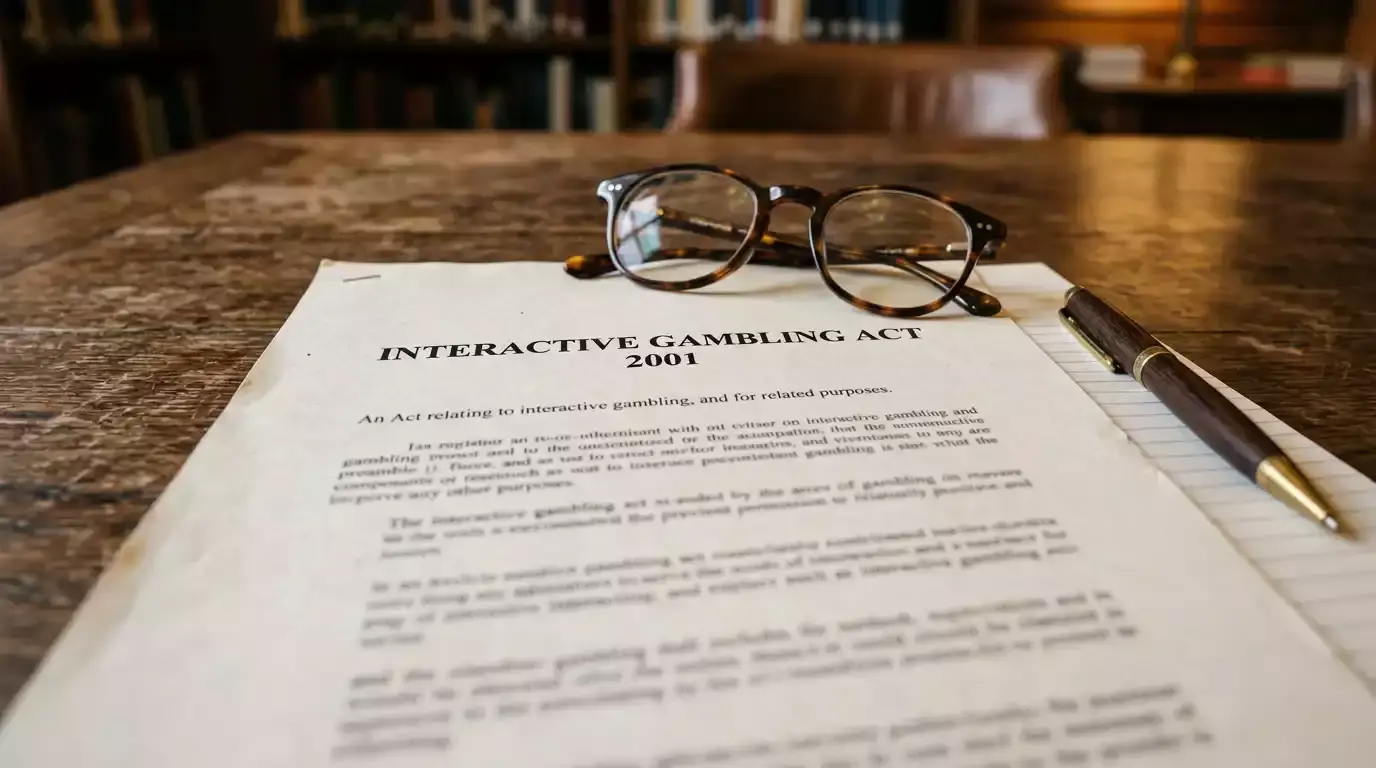

The Interactive Gambling Act 2001 makes it illegal for operators to offer real-money online casino games to Australian residents. The law targets the supply side — the casino, not the player. No Australian has been prosecuted for using an offshore casino. But the regulatory environment has shifted dramatically since 2023, and the trend line points toward increasing enforcement pressure, not less.

Amanda Rishworth, Australia’s Minister for Social Services, was direct when she explained the rationale behind the credit card and crypto ban: the government takes seriously its responsibility to prevent and reduce harm from online wagering, and the same rules that apply to land-based gambling now apply online. That ban, effective since June 2024, carries penalties of up to A$234,750 for operators that violate it. The ban covers credit cards and cryptocurrency at licensed wagering services — but critically, most online casinos operating in Australia are not licensed here. They hold licences from Curaçao, Malta, or other offshore jurisdictions, which means the Australian ban does not technically apply to them.

Here is where it gets complicated. ACMA — the Australian Communications and Media Authority — has blocked 1,708 illegal gambling and affiliate websites as of May 2026. More than 230 additional illegal services have voluntarily exited the Australian market under regulatory pressure. That enforcement is accelerating, not slowing down. If you are using crypto at an offshore casino and that casino gets blocked by ACMA, your funds may become inaccessible without any recourse. PayID deposits at the same offshore casino carry the same risk of the site being blocked, but the banking trail makes it easier to pursue a dispute through your bank if the operator disappears.

The practical difference: PayID creates a documented paper trail through your bank. Every transaction is linked to your identity, your bank account, and a timestamp. Crypto, while not truly anonymous, is pseudonymous — the trail exists on the blockchain but is not automatically linked to your real identity unless you used a KYC-verified exchange. For players who value regulatory compliance and the ability to dispute transactions, PayID is the lower-risk option. For players who accept the trade-offs of operating outside the licensed ecosystem, crypto offers more flexibility — but with fewer protections if things go wrong.

I should be clear about one thing: I am a payments analyst, not a lawyer. The legal landscape around alternative payment methods at online casinos is evolving rapidly, and anyone with concerns about their specific situation should seek independent legal advice.

Where PayID Has the Edge

Three months ago I was consulting for a payment services provider that handles transaction routing for mid-sized casino operators. The data they shared confirmed what I had suspected from anecdotal observation: Australian players overwhelmingly prefer PayID when given both options. The reason was not speed or fees — it was simplicity.

PayID requires zero additional setup beyond what most Australians already have. If you have a bank account with any of the 110-plus NPP-connected institutions, you can deposit at a PayID casino in under two minutes. No exchange account, no wallet software, no seed phrases, no gas fee calculations. You open your banking app — the same one you use to pay rent and split dinner bills — enter the casino’s PayID, and send. Australia’s total payments market is projected to reach US$2.29 trillion by 2030, and PayID is positioned at the centre of that growth precisely because it removes friction from the equation.

The native AUD support eliminates currency risk entirely. When you deposit A$200, the casino receives A$200. When you withdraw A$500, your bank account shows A$500. There is no conversion spread, no exchange rate fluctuation, no scenario where the value of your deposit changes while it is in transit. For recreational players who deposit and withdraw in the same currency, this predictability is worth more than the theoretical speed advantage of blockchain settlement.

PayID also integrates naturally with responsible gambling controls. Because transactions flow through your bank, every deposit and withdrawal appears in your bank statement. You can set up spending alerts, track monthly gambling expenditure through your banking app, and use bank-level transaction controls to limit outgoing payments. Crypto wallets do not offer these built-in oversight features — and for players who want to maintain visibility over their gambling spending, that integration is a genuine safety advantage.

Finally, dispute resolution. If a PayID casino fails to credit your deposit or refuses a legitimate withdrawal, you have a documented trail through your bank and can escalate through your bank’s complaints process, the Australian Financial Complaints Authority, or ACMA. Crypto transactions offer none of these avenues. Once a Bitcoin transaction confirms, no intermediary can intervene on your behalf.

Where Crypto Still Leads

I would be doing you a disservice if I pretended PayID beats crypto on every metric. It does not. There are specific scenarios where cryptocurrency remains the superior payment method, and glossing over them would undermine the analytical credibility of everything else in this article.

Privacy is the most obvious advantage. PayID attaches your legal name to every transaction and creates a permanent record in your bank’s systems. Crypto, used carefully, separates your real-world identity from your gambling activity. For players who do not want casino transactions appearing on bank statements — whether for personal privacy, family reasons, or simply because they view gambling as a private matter — crypto provides a layer of separation that PayID structurally cannot offer.

Transaction limits favour crypto as well. There is no bank-imposed daily cap on a Bitcoin transfer. A player can deposit A$50,000 in a single transaction if the casino’s wallet accepts it. PayID’s bank-level caps, while adjustable, create an additional step for high-value deposits that crypto eliminates entirely. For VIP players or anyone moving significant sums, that ceiling matters.

Speed on the withdrawal side gives crypto a narrow edge at the pure settlement layer. Once a casino broadcasts a crypto withdrawal, blockchain confirmation is independent of business hours, banking relationships, or payment network intermediaries. PayID is also 24/7, but the casino’s internal processing still gates the release. At operators that are slow to process, crypto and PayID withdrawals wait in the same internal queue — but once released, crypto arrives without touching any banking infrastructure that could introduce delay.

Global portability is another factor. PayID is an Australian system. It works with Australian banks and Australian dollars. If you travel internationally or maintain gaming accounts with operators that do not accept AUD, crypto works the same everywhere. A Bitcoin deposit from a hotel in Tokyo settles at the same speed and with the same process as one from Sydney. PayID stops at the Australian border.

And then there is access. The June 2024 ban removed crypto from licensed operators, but it simultaneously highlighted that the largest volume of online casino activity in Australia happens at unlicensed offshore sites — sites that ACMA is actively blocking but that continue to operate and accept Australian players. At these sites, crypto is often the smoothest payment experience because it bypasses Australian banking infrastructure entirely, avoiding the bank-level blocks on gambling transactions that some Australian institutions have quietly implemented.

None of these advantages come without cost. Crypto’s privacy means weaker dispute resolution. Its lack of limits means no bank-level safety net if you overspend. Its global portability means no local regulatory body has jurisdiction over your funds. Every advantage has a corresponding risk, and the calculation is personal. What I can say, from years of watching players navigate both systems, is that the players who do best with crypto are those who understand blockchain mechanics, maintain disciplined bankroll management, and accept the absence of institutional protections as a conscious trade-off rather than an afterthought.

The players who do best with PayID are those who value the predictability of Australian dollars, the transparency of bank statements, and the ability to pick up the phone and call their bank if something goes wrong. Neither group is wrong. They are optimising for different outcomes.