A player I advised last year won A$4,200 on a Saturday night and immediately requested a withdrawal via PayID. He expected the money in his bank account within minutes — after all, the casino’s homepage promised “instant withdrawals.” Fourteen hours later, he was still waiting. The funds arrived Sunday morning, which by any historical standard is remarkably fast, but it was not the “instant” he had been sold.

That gap between marketing language and mechanical reality is exactly what this article addresses. PayID casino instant withdrawal is a phrase you will see on virtually every operator that accepts the method, and it is not entirely dishonest — the payment itself, once released, settles in seconds through the NPP’s real-time infrastructure. The NPP processes over 155 million payments every month at that speed. But the casino’s internal processing — fraud checks, KYC verification, wagering requirement audits, manual approval queues — adds hours, sometimes a full day, before the operator even sends the payment.

I have spent eight years watching the payment side of iGaming in Australia, and the withdrawal experience is where player expectations and operational reality collide most violently. Every quarter, I review cash-out data from multiple operators, and the patterns are remarkably stable: the same structural bottlenecks appear regardless of the operator’s size, jurisdiction, or the flashiness of their marketing. The payment rail is never the problem. The casino always is.

So here is the honest picture: what “instant” actually means in the context of PayID withdrawals, what slows the process down, and the specific steps you can take to position yourself for the fastest possible cash-out. No sugarcoating, no operator cheerleading — just the mechanical truth about getting your money from a casino balance to your bank account.

What “Instant Withdrawal” Actually Means at PayID Casinos

Last month I timed withdrawals at three different operators over the course of a week, just to get current data for a client. The fastest was eleven minutes from request to bank account. The slowest was nine hours. Same payment method, same bank, same player profile. The variable was not PayID — it was the casino.

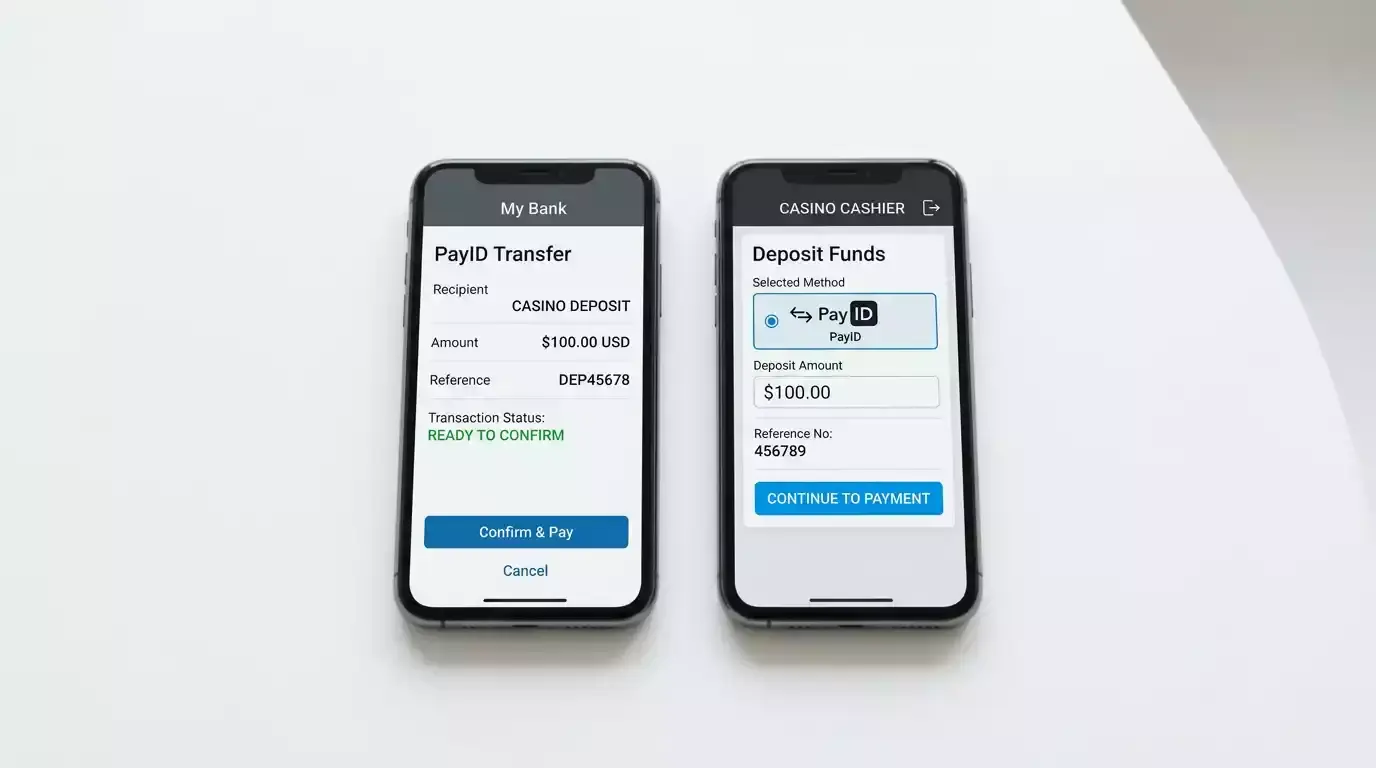

To understand why, you need to separate the two stages of a PayID withdrawal. Stage one is the operator’s processing pipeline. When you submit a withdrawal request, the casino queues it for internal review. A compliance team — or an automated system, at larger operators — checks that you have met the wagering requirements on any active bonus, verifies your identity if this is your first withdrawal, confirms that the withdrawal amount falls within the operator’s daily and weekly limits, and screens the transaction for anti-money laundering flags. This stage can take anywhere from five minutes to twenty-four hours, depending entirely on the operator’s staffing, automation level, and compliance posture.

Stage two is the actual PayID transfer. Once the casino approves the withdrawal and initiates the payment through the NPP, settlement is genuinely instant. Anna Bligh, the former CEO of the Australian Banking Association, highlighted one of PayID’s key features when she noted that the system shows a confirmation screen — including the intended recipient’s name — before a payment is finalised. That same mechanism works in reverse for withdrawals: the casino sends to your registered PayID, the NPP routes it in real time, and the money appears in your bank account within seconds. No batch processing, no overnight clearing, no weekend delays on the payment rail itself.

So when an operator says “instant PayID withdrawal,” they are technically describing stage two accurately. The problem is that stage one — their own internal processing — is where all the waiting happens. And most marketing material conveniently omits that part.

In practice, here is what I tell players to expect. Operators with fully automated compliance systems and 24/7 processing teams can turn around a PayID withdrawal in ten to thirty minutes. Mid-tier operators with partial automation typically process within two to six hours. Operators that rely on manual review, especially those with small compliance teams operating in a single time zone, can take twelve to twenty-four hours. All of these assume you have already completed KYC verification and have no pending bonus wagering requirements — two conditions that, if unmet, can add days rather than hours.

One detail that surprises many players: NPP operates 24/7, 365 days a year. There is no “banking hours” limitation on the payment rail. If the casino releases your withdrawal at 2 a.m. on a public holiday, the money still settles in your account instantly. The bottleneck is never the NPP. It is always the operator.

This distinction matters because it reframes the question entirely. When you are evaluating operators for withdrawal speed, you are not evaluating PayID — PayID is constant. You are evaluating the casino’s internal operations. How large is their compliance team? Do they operate around the clock or only during business hours in a single time zone? Have they invested in automated payment processing, or does every withdrawal sit in a queue waiting for a human to click “approve”? These operational details are rarely advertised, but they are the only variables that determine how long you actually wait.

I have seen a growing trend of operators publishing average withdrawal times on their banking pages — “average PayID processing: 47 minutes” — which is a step in the right direction. Take those numbers with appropriate scepticism, since they are self-reported and may not include outlier delays, but they are better than the vague “instant” label that most sites still default to.

Five Factors That Slow Down Your PayID Cash-Out

Not every withdrawal delay is the casino dragging its feet. Some are structural, some are regulatory, and some are entirely within your control. Here are the five I encounter most frequently, in rough order of how often they cause problems.

1. Incomplete KYC verification

If you have not completed identity verification before requesting your first withdrawal, the operator is legally obligated to hold your funds until you do. This means uploading government-issued ID, proof of address, and sometimes a selfie holding your ID. At some operators, KYC review takes hours. At others, it stretches to three business days. The timeline depends on whether the casino uses automated document verification software or relies on a human compliance officer reviewing each submission manually.

The fix is simple: complete verification immediately after registration, long before you have winnings to withdraw. Operators that process KYC at the deposit stage rather than the withdrawal stage tend to have faster cash-outs across the board. I have seen players lose access to time-sensitive bonus offers because their withdrawal was stuck in KYC limbo for 72 hours — all because they skipped a five-minute upload process when they first signed up.

2. Unmet wagering requirements

You accepted a deposit bonus with a 35x wagering requirement. You have played through 28x. The casino will not release a withdrawal until the requirement is either fully met or the bonus is forfeited. This is not a PayID issue — it applies to every payment method — but it catches players who forget they have an active bonus. Check your bonus status in the casino’s promotions or account section before requesting a withdrawal.

3. AML and regulatory compliance checks

Since June 2024, Australian regulations have tightened around online gambling payments, including the ban on credit card and cryptocurrency transactions at licensed operators. That regulatory environment means operators are more cautious, not less, about outgoing payments. Large withdrawals — particularly those above A$10,000 — trigger additional AML screening. The operator may ask for source-of-funds documentation, a process that can add one to three days. This is not the casino being difficult; it is the casino staying on the right side of AUSTRAC requirements. The A$450 million fine imposed on Crown Resorts for systemic AML failures serves as a reminder of how seriously regulators treat non-compliance.

4. Operator processing schedules

Some casinos process withdrawals in batches — twice a day, three times a day, or in some cases once a day during a specific window. If you submit a request at 3 p.m. and the next batch runs at 9 a.m. the following morning, your withdrawal sits in the queue for eighteen hours regardless of how fast PayID itself operates. Operators with real-time or rolling processing are faster, but not all of them advertise their schedule transparently. If withdrawal time is a priority for you, contacting support before your first cash-out to ask about their processing cadence is worth the effort.

5. Withdrawal reversal windows

Some operators impose a “pending period” — typically 24 to 72 hours — during which you can cancel a withdrawal and return the funds to your casino balance. This is framed as a player convenience feature, but it also serves the operator: during the pending period, you might reverse the withdrawal and keep playing. The psychology is deliberate. A pending balance feels less “final” than money in your bank account, and a non-trivial percentage of players do reverse withdrawals and continue wagering.

Not all operators have this policy, and those that do not will generally process your cash-out faster. If your withdrawal shows as “pending” with a cancel option, the clock on processing has not even started yet. Look for operators that either have no reversal window or offer an option to waive it in your account settings. Some sites let you disable the pending period permanently, which removes the temptation and speeds up every future withdrawal.

How to Get Your Winnings Faster

I once helped an operator redesign their withdrawal pipeline and cut average processing time from eight hours to forty-five minutes. The changes were all on the casino’s backend, and as a player you cannot do that. But you can eliminate every delay that depends on you. Here is what I have seen work, over hundreds of cash-outs.

Complete KYC verification on the day you register. Upload your ID, proof of address, and any other documents the operator requests. Do not wait until you have winnings — do it when the stakes are zero and you have no reason to feel rushed. Some operators even offer expedited verification if you submit documents within the first 24 hours of account creation.

Clear or forfeit any active bonus before requesting a withdrawal. If you are close to meeting the wagering requirement, play it out. If you are nowhere near it, consider forfeiting the bonus entirely so the withdrawal is not blocked. Many players do not realise that forfeiting a bonus also forfeits the bonus funds — but it releases your deposited funds and any winnings earned from them, which is often a better outcome than grinding through unachievable wagering targets.

Time your withdrawal request. If the operator processes in batches, try to submit just before the next batch runs. If you do not know their schedule, submit in the morning during Australian business hours. Operators with compliance teams in Australian or Southeast Asian time zones tend to process faster during their working day — requests submitted at midnight AEST sit in queue until the team starts work.

Avoid round-number withdrawals above A$10,000. Transactions at or above this threshold are more likely to trigger enhanced AML checks. If you have A$12,000 to withdraw, consider splitting it into two requests of A$6,000 each — though be aware that structured splitting to avoid thresholds can itself raise flags if the pattern is obvious. The goal is not to evade checks; it is to keep individual transactions within the range that automated systems can approve without escalation.

Choose operators with a track record of fast processing. Player forums, independent review sites, and community discussions are better indicators of real withdrawal speed than anything on the casino’s own website. An operator that consistently processes within two hours will do so for your withdrawal too. An operator with a history of 48-hour delays will not magically speed up for you.

One more tactic that I have found surprisingly effective: contact live chat after submitting your withdrawal and politely ask them to expedite the review. At operators with manual processing, a support agent can flag your request and move it up the queue. This does not work at sites with fully automated pipelines — there is no human to nudge — but at mid-tier operators with hybrid systems, a thirty-second chat interaction can shave hours off your waiting time. It is not glamorous advice, but it works.

Finally, keep your account details consistent. If your PayID display name, your casino account name, and your submitted KYC documents all match exactly, the automated compliance system has nothing to query. Discrepancies — a middle initial in one place but not another, a shortened first name, a recently changed surname — create friction points that can trigger manual review. Consistency is the unglamorous foundation of fast withdrawals.

PayID Payout Speed vs Other Methods

Numbers tell this story better than paragraphs. I have tracked withdrawal speeds across payment methods for years, and while individual operator variation is significant, the pattern is consistent.

PayID withdrawals, once released by the operator, settle in seconds. Total time from request to bank account — including casino processing — typically ranges from two to twelve hours. The NPP rail adds zero delay.

Debit and credit card withdrawals follow traditional card network clearing. Even after the casino releases the payment, the card network’s settlement process takes one to five business days. Part of the reason is fraud infrastructure: card payment fraud in Australia hit A$854 million in FY25, and the layers of screening built into the card network’s pipeline add processing time at every stage. PayID’s dramatically lower fraud footprint — A$260,000 in PayID-specific scams reported in 2023 versus that A$854 million in card fraud — means fewer checks and faster clearing.

Cryptocurrency withdrawals are the fastest in pure settlement terms. Once an operator broadcasts a Bitcoin or Ethereum transaction to the blockchain, confirmation takes minutes to an hour depending on network congestion and the number of confirmations the casino requires. However, the casino’s processing time before broadcast is comparable to PayID — same KYC checks, same AML screening. And with licensed Australian operators now banned from processing crypto transactions since June 2024, this option is only available at offshore sites, which carry their own set of risks.

E-wallet withdrawals to services like Neteller or Skrill typically take 24 to 48 hours total. The e-wallet provider adds its own processing layer between the casino and your bank, and withdrawing from the e-wallet to your Australian bank account adds another one to three business days on top.

Bank wire transfers — the traditional method — remain the slowest, often taking three to seven business days. They are also the most expensive, with some operators charging A$20 to A$50 per wire transfer. For all their drawbacks, wires do handle large sums without the daily caps that constrain PayID and card withdrawals — which is why some high-volume players still use them for five-figure cash-outs despite the wait.

One factor that rarely gets mentioned in speed comparisons is what happens when something goes wrong. A failed or disputed card withdrawal can take weeks to resolve through the card network’s chargeback process. A disputed e-wallet withdrawal adds the e-wallet provider as a third party in the dispute, compounding the timeline. PayID, by contrast, settles irrevocably — if the casino sends it and the NPP delivers it, the money is in your account and there is no intermediary to dispute through. That finality cuts both ways, but for legitimate withdrawals it means fewer complications and no clawback risk after settlement.

The bottom line is straightforward. For Australian players who want winnings in their bank account as fast as possible without using offshore-only methods, PayID offers the shortest realistic path. It is not truly instant — that word should be retired from casino marketing — but it is faster than every other method available at Australian-facing operators by a significant margin.