More than 27 million PayID registrations exist in Australia as of mid-2025, and that number continues to climb. Meanwhile, POLi — the other bank-based payment option you will find at many Australian-facing casinos — operates on fundamentally different infrastructure with a different set of trade-offs. I have tested both methods across dozens of operators, and the comparison is not as one-sided as you might assume if you only read PayID marketing materials.

Both methods move money from your Australian bank account to a casino balance without requiring card details. But the mechanisms, speeds, security models, and long-term prospects diverge significantly. This breakdown covers the practical differences so you can choose the method that fits your priorities.

Feature-by-Feature Comparison: PayID and POLi

I ran a head-to-head test last year that illustrates the core difference. I deposited AU$50 at the same operator using both methods within 30 minutes of each other. The PayID deposit cleared in 11 seconds. The POLi deposit took about 90 seconds — still fast, but the experience was qualitatively different.

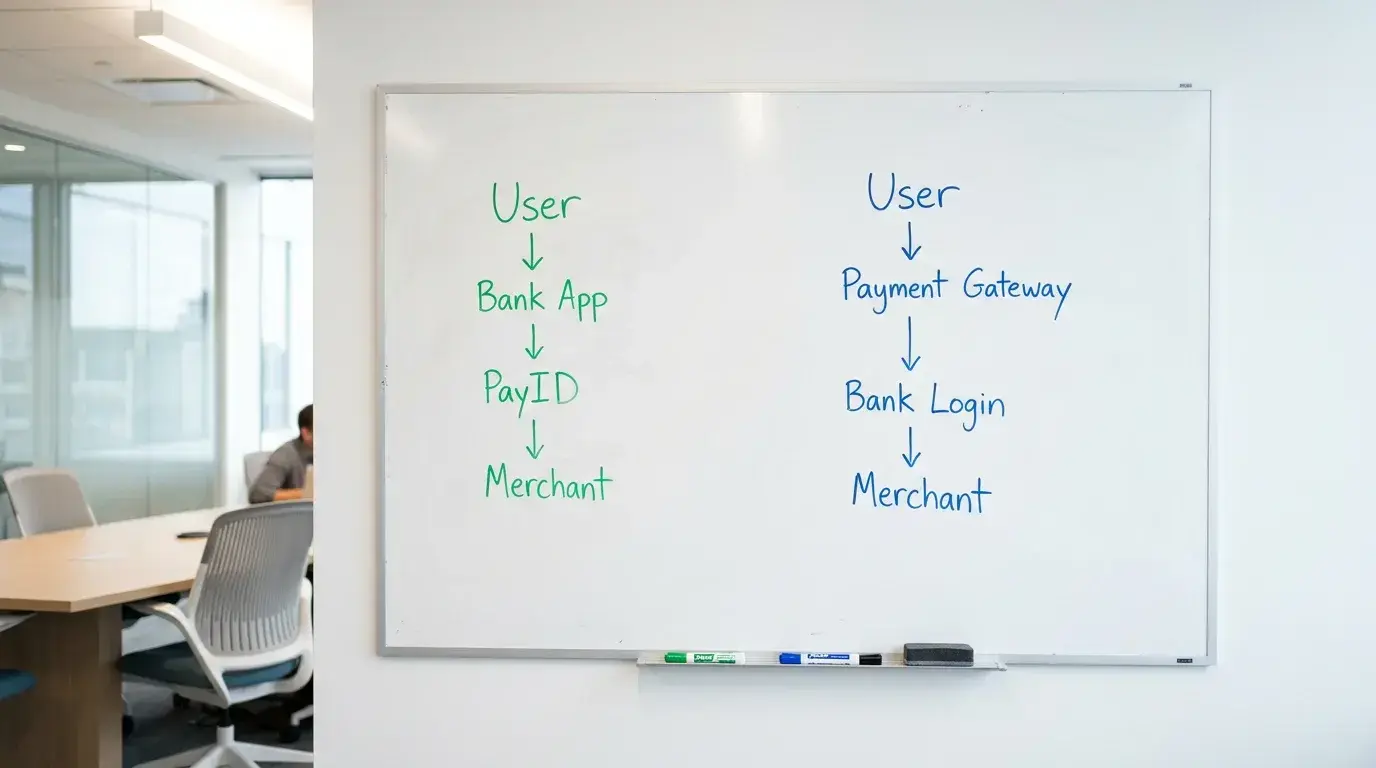

PayID works by sending a real-time payment through the NPP, which processes over 155 million transactions monthly. You enter the casino’s PayID (email or phone number), confirm the recipient name on the verification screen in your banking app, enter the amount, and authorise. The funds transfer instantly, and the casino credits your balance within seconds. The process is a push payment — you initiate and control it from your banking app.

POLi works differently. When you select POLi at a casino’s deposit page, you are redirected to POLi’s intermediary platform, which opens a secure session with your online banking portal. You log into your bank through POLi’s interface, select the account to pay from, and POLi facilitates a direct bank transfer. The payment is technically a standard bank transfer processed through POLi’s system, not a real-time NPP payment. This means POLi deposits can take a few minutes to reflect in your casino balance, though most complete within one to five minutes.

Speed: PayID is faster. Seconds versus minutes. For most players, this difference is negligible in practice — you are not going to notice a three-minute delay. But if you are trying to top up mid-session during a live dealer game, those extra minutes can matter.

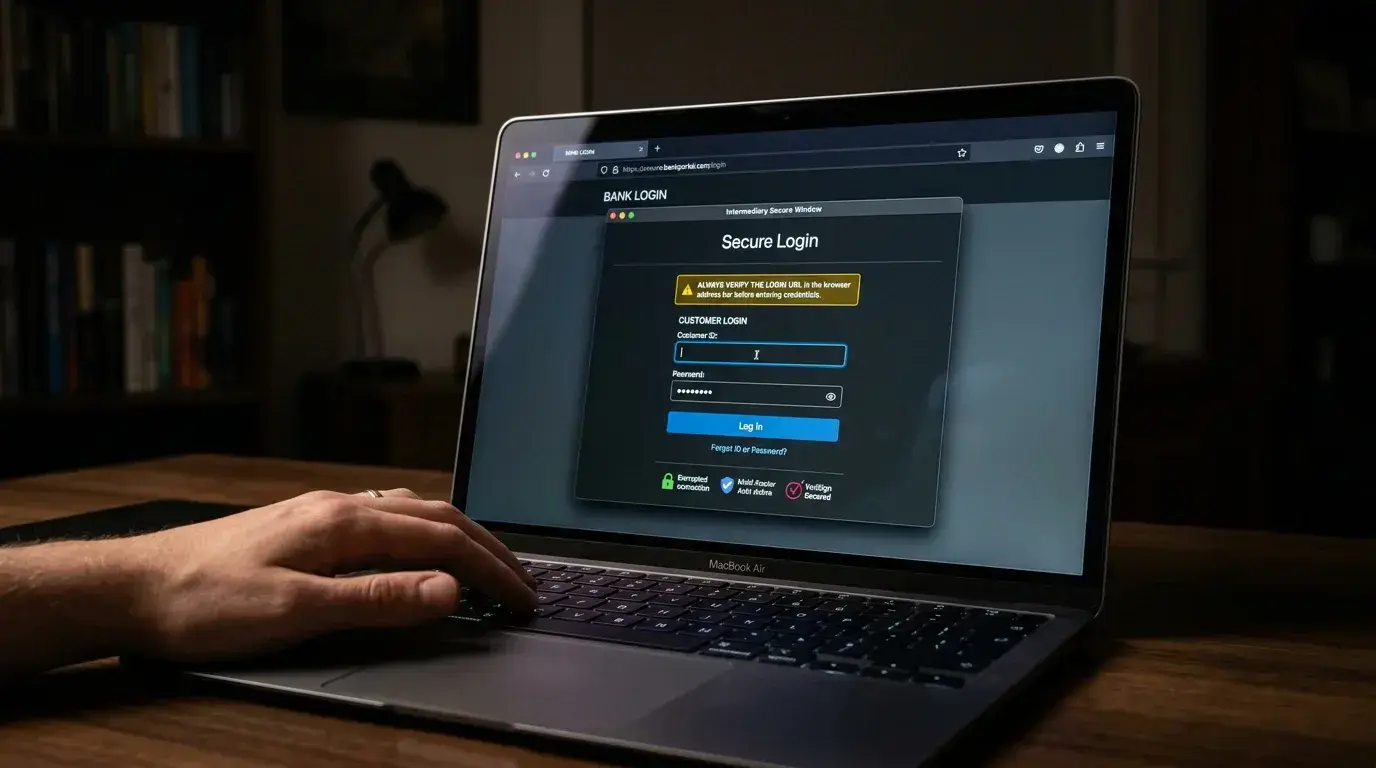

Security model: This is where the comparison gets interesting. PayID never requires you to enter your banking credentials into any third-party system. You stay within your bank’s own app the entire time. POLi requires you to log into your bank’s online portal through POLi’s intermediary window. POLi insists this process is secure and does not store your credentials, but several Australian banks have expressed discomfort with the model. Some banks have restricted or warned against POLi usage specifically because it involves entering banking credentials into a non-bank interface.

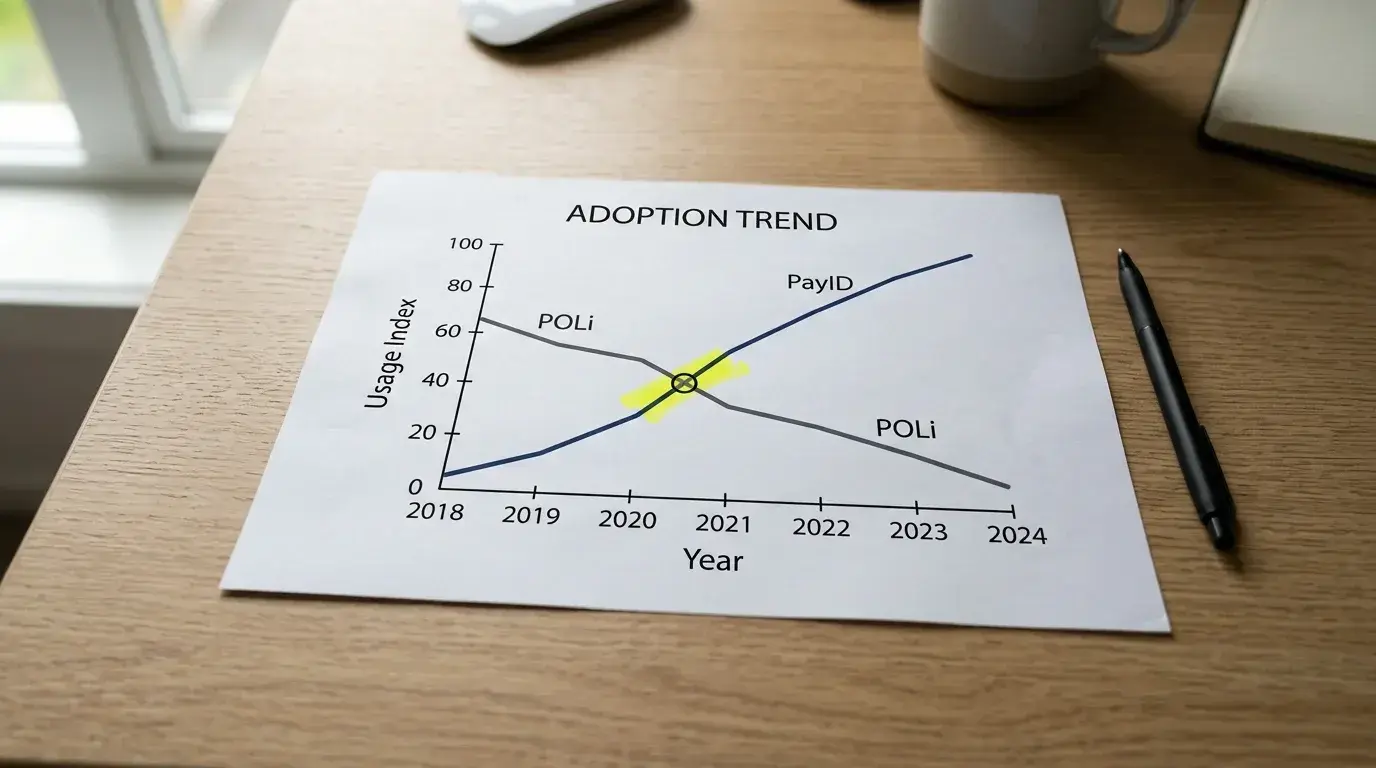

Availability: POLi has been around longer and is still accepted at many operators that have not yet added PayID. However, the trend is moving in one direction. As PayID adoption grows and banks continue to invest in NPP integration, the number of operators adding PayID as a deposit method is increasing, while POLi’s market share is gradually declining.

Withdrawals: PayID supports both deposits and withdrawals — you can receive funds from the casino directly into your bank account via your PayID. POLi, by design, is a deposit-only method. You cannot withdraw through POLi. This means POLi depositors must use an alternative method for withdrawals, which adds a layer of complexity that PayID users avoid.

Fees: Both methods are free at the consumer level for deposits. Neither PayID nor POLi charges you a transaction fee. The casino may apply its own processing fee regardless of method, but this is operator-specific and not tied to the payment rail.

When to Use PayID and When POLi Still Makes Sense

The broader payment comparison covers additional methods including cryptocurrency, but within the bank-transfer category, the choice between PayID and POLi comes down to three practical factors.

Use PayID when your primary concern is speed, security, or withdrawal convenience. The instant processing, the confirmation screen that verifies the recipient before you send, and the ability to withdraw back to your bank through the same method make PayID the more complete option. If your bank supports PayID — and at 110+ participating institutions, it almost certainly does — there are few practical reasons to choose POLi over PayID for new deposits.

POLi still makes sense in specific situations. Some operators that serve the Australian market have not yet integrated PayID into their deposit systems. If your preferred casino offers POLi but not PayID, POLi remains a viable bank-based deposit method that avoids the need for card numbers. It is also the more familiar option for players who have used it for years and are comfortable with the intermediary login process.

The longer-term outlook favours PayID. POLi’s model of intermediary bank logins is increasingly at odds with the direction of Australian banking security. Banks are investing in their own payment apps and APIs, and the trend is toward methods where customers authenticate directly through their bank rather than through third-party interfaces. PayID aligns with this direction. POLi’s relevance depends on whether it adapts its model or whether the market moves past it entirely.

One scenario where both methods coexist usefully: maintaining a backup option. If your bank occasionally flags or delays PayID transfers to a specific operator, having POLi as an alternative deposit method means you are not locked out of a session. Payment diversity is a practical consideration that most guides overlook — relying on a single deposit method creates a single point of failure.