Over 114 million accounts are connected to the New Payments Platform in a country of 26 million people — roughly four accounts per person. That statistic alone tells you something about the scale of the infrastructure sitting beneath every PayID casino deposit. Most players interact with PayID as a simple feature in their banking app, but the system underneath is a multi-layered real-time payment network that fundamentally changed how money moves in Australia.

Understanding these layers is not academic. When your casino deposit takes three seconds instead of two days, or when your withdrawal processes on a Sunday afternoon instead of waiting until Monday, those outcomes are direct results of NPP architecture. This guide explains the system in practical terms.

How the New Payments Platform Processes Casino Transactions

Anna Bligh, then CEO of the Australian Banking Association, put the NPP’s significance in context when she noted that Australia was using a 60-year-old system for many everyday payments. The NPP replaced that legacy infrastructure with a platform capable of processing payments in real time, 24 hours a day, 365 days a year — including weekends and public holidays.

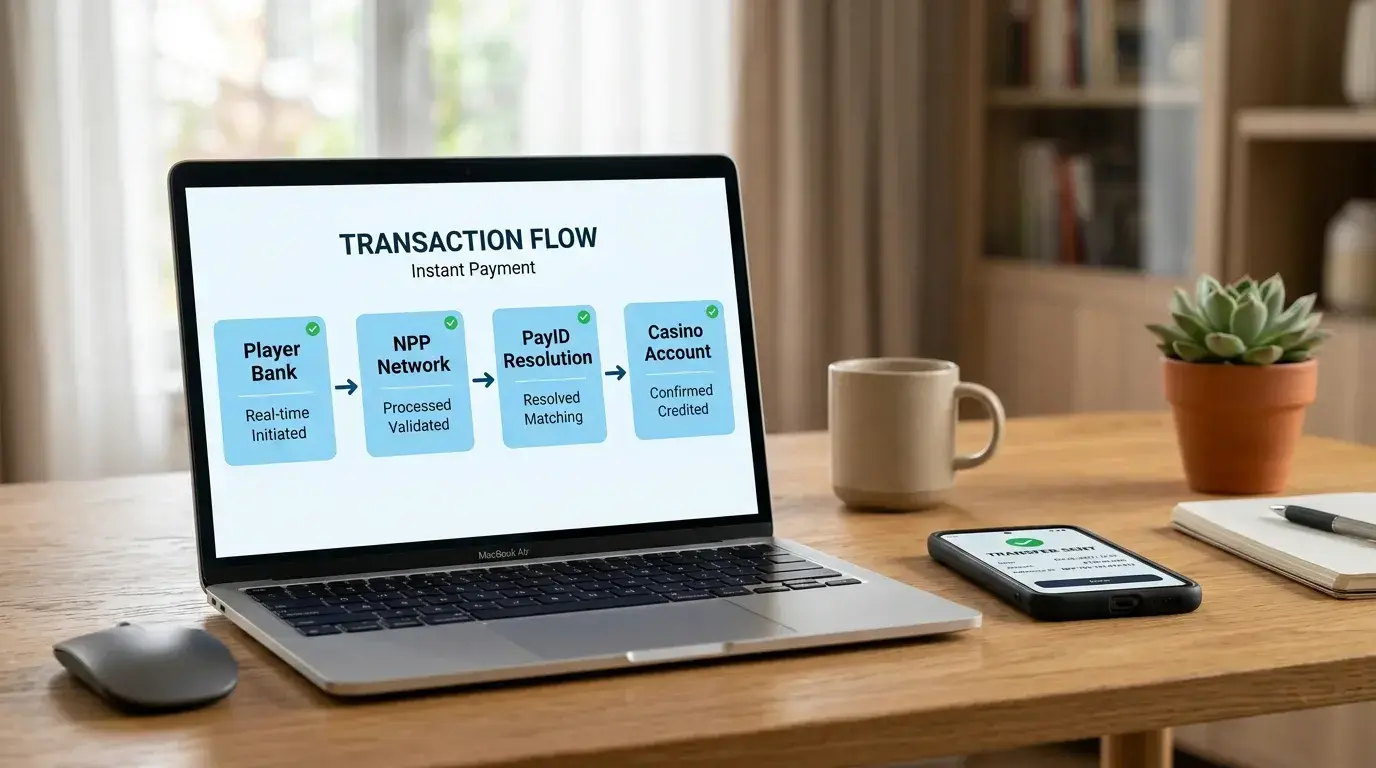

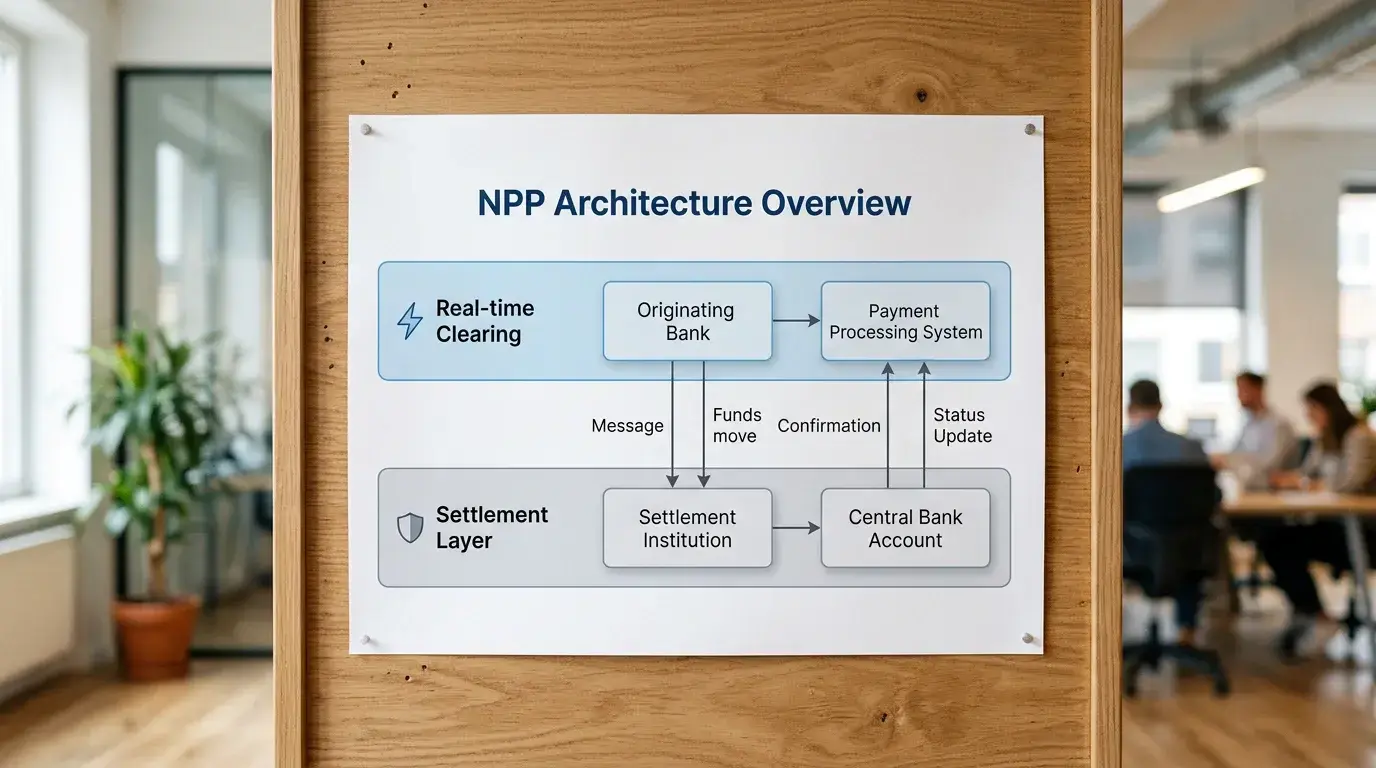

The NPP operates on three layers. The Basic Infrastructure layer handles the core messaging and clearing between banks. When you initiate a PayID transfer to a casino, your bank sends a payment instruction through this layer to the recipient’s bank. The instruction includes the amount, the sender’s details, and the PayID of the recipient. The recipient bank validates the instruction, credits the recipient’s account, and sends a confirmation back — all within seconds.

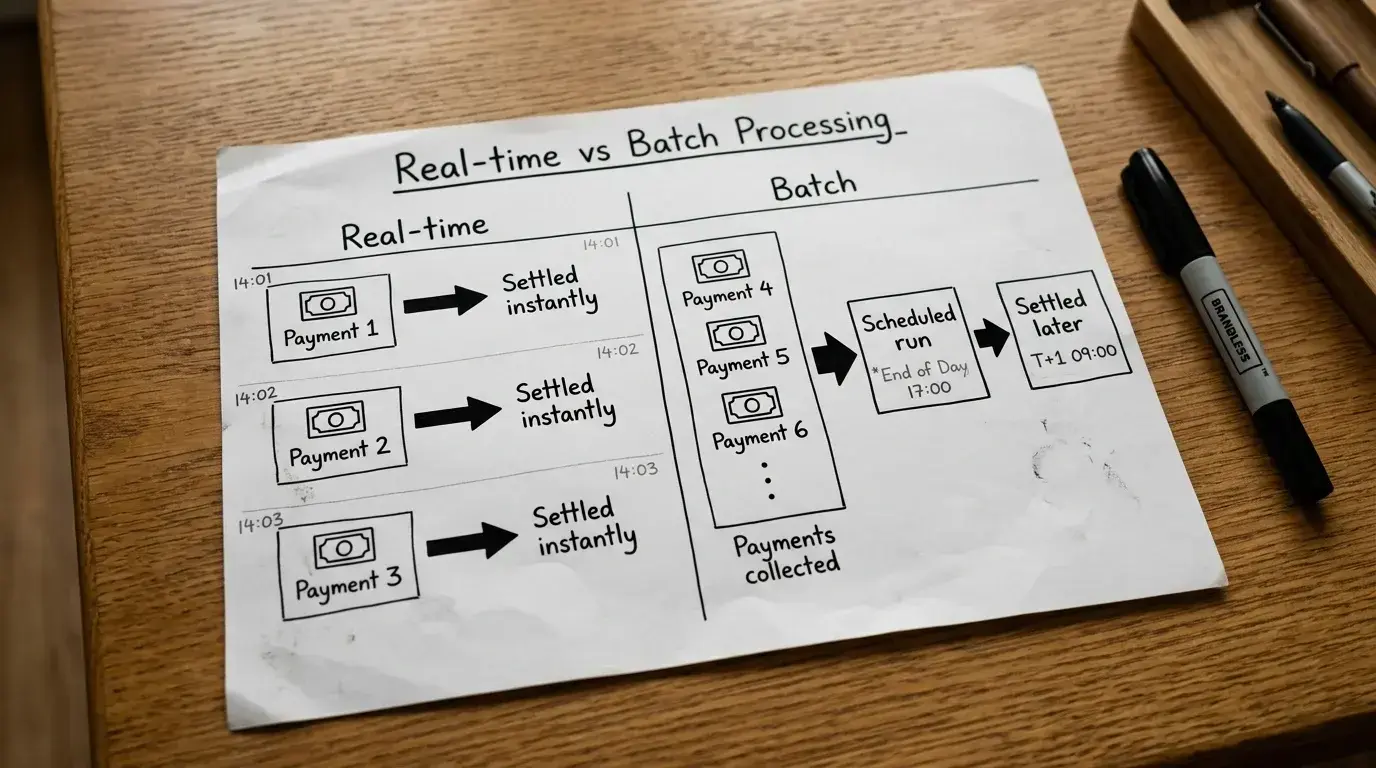

The NPP processes more than 155 million real-time transactions every month through this infrastructure. Each transaction settles individually in real time through the Reserve Bank of Australia’s Fast Settlement Service, rather than being batched and netted like traditional bank transfers. This individual settlement is why PayID payments are genuinely instant — the money moves, clears, and settles in one continuous process.

The second layer is the overlay services — commercial products built on top of the Basic Infrastructure. Osko is the primary overlay service for consumer payments. When your banking app says it is sending a PayID payment, Osko is the messaging protocol that makes it happen. Osko defines the payment message format, enables the confirmation screen that shows the recipient’s name, and handles the data payload that accompanies each transaction.

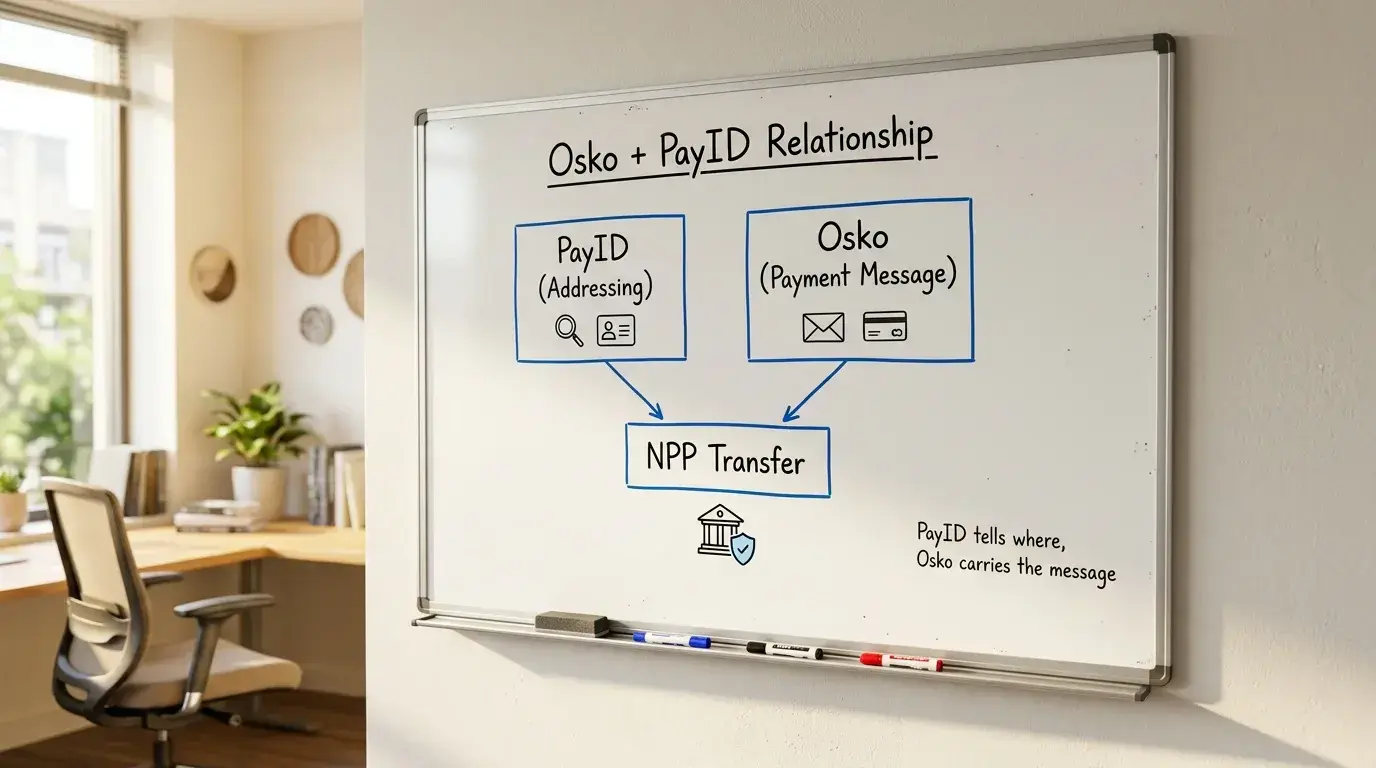

Osko and PayID: Two Layers of the Same System

The relationship between Osko and PayID confuses many players because the terms are used interchangeably in some contexts and distinctly in others. Here is the clearest way to understand it: PayID is the addressing system — it maps your phone number or email to a bank account. Osko is the messaging service — it carries the payment instruction across the NPP. You need both for a real-time casino deposit, but they serve different functions.

When you type a casino’s PayID into your banking app, the app uses the NPP’s PayID lookup service to resolve that identifier to a specific bank and account number — without showing you those raw details. Osko then carries the payment instruction, including the amount and any reference data, from your bank to the casino’s bank. The casino’s bank credits the operator’s account, and the casino’s system detects the incoming payment and credits your player balance.

For casino players, the practical implication is reliability. Because the NPP operates continuously, your deposit does not depend on batch processing windows. A Saturday night deposit arrives just as quickly as a Tuesday afternoon one. Withdrawals, however, are still subject to the casino’s internal processing schedule — the NPP is instant, but the operator’s compliance review is not.

The banking support guide covers which institutions are connected to the NPP and any bank-specific considerations for gambling transactions.