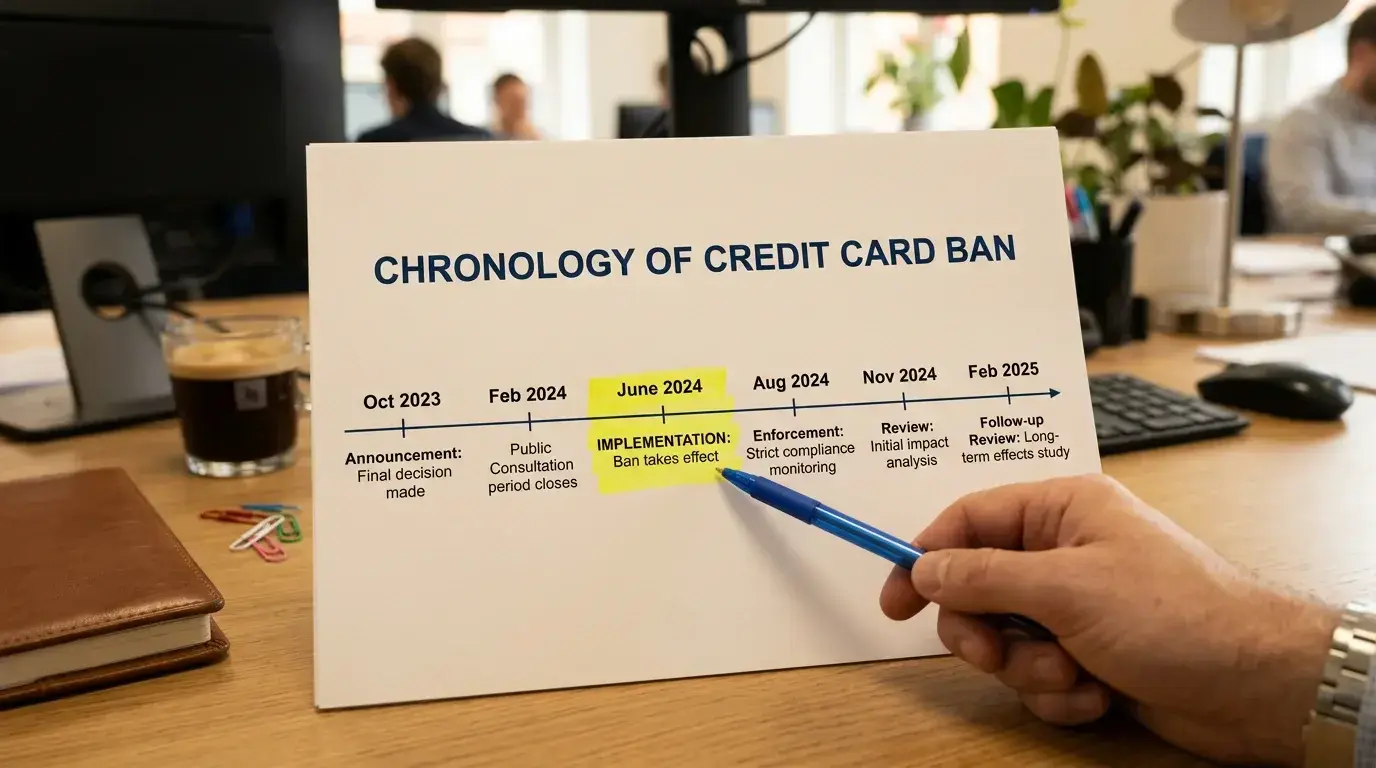

On 11 June 2024, Australia banned the use of credit cards and cryptocurrency for online wagering at licensed operators. The penalty for non-compliance: up to AU$234,750. I had been tracking the legislative progress of this ban for months before it took effect, and the immediate aftermath reshaped the payment landscape at Australian-facing casinos faster than any regulatory change I have seen in my career. PayID, already growing rapidly, became the default payment method for a large segment of the market almost overnight.

This was not accidental. The ban removed two major deposit options simultaneously — credit cards and crypto — while leaving debit cards, bank transfers, and PayID untouched. Understanding what the ban covers, what it does not, and how it redirected payment flows toward PayID is essential context for anyone depositing at online casinos in 2026.

What the Credit Card Ban Covers — and What It Does Not

Minister for Communications Michelle Rowland framed the policy in stark terms: Australians should not be gambling with money they do not have. That single sentence captures the rationale. Credit card gambling allows people to wager borrowed money — money they must repay with interest regardless of whether they win or lose. The ban removes that option at licensed Australian operators.

The scope is specific. The ban applies to interactive wagering services licensed in Australia — primarily sports betting operators regulated by state and territory authorities. It prohibits credit card deposits for placing bets. It also extends to cryptocurrency, which was simultaneously banned as a deposit method at licensed operators. The penalty framework targets operators who continue to accept prohibited payment methods, not individual players who attempt to use them.

What the ban does not cover is equally important. Debit cards remain legal for gambling deposits. Bank transfers — including PayID — remain legal. E-wallets funded from a bank account (not a credit line) remain legal. The ban targets the source of funds (credit) and the anonymity of certain methods (crypto), not the act of digital payment itself. Card fraud data provides context for the broader payment risk environment: Australian card fraud reached AU$854 million in FY25, though it declined slightly from AU$868 million the previous year, with a fraud rate of 71.8 cents per AU$1,000 spent.

Offshore operators — the unlicensed casinos that most PayID casino players use for pokies and table games — are technically outside the ban’s enforcement scope. ACMA does not regulate offshore operators’ payment methods because those operators are not licensed in Australia in the first place. Some offshore casinos continue to accept credit cards and crypto from Australian players. However, Australian banks independently monitor and flag transactions that appear to violate the spirit of the ban, even when the recipient is offshore. Several major banks have implemented their own restrictions on credit card transactions coded as gambling, regardless of the operator’s licensing status.

How PayID Filled the Gap Left by Credit Cards

The payment redistribution after the ban was measurable within weeks. Players who had been using credit cards needed an alternative that was fast, free, and integrated with their existing banking setup. PayID met all three criteria. A debit card deposit works too, but PayID offers a faster processing time (seconds versus minutes to hours for some card transactions) and avoids the need to enter card details at the casino’s checkout page.

The structural advantage of PayID in a post-credit-card world is that it forces players to use funds they already have. Every PayID payment comes directly from a bank account balance — there is no credit line attached, no interest accruing, no repayment schedule. This aligns with the policy intent of the ban even at operators that sit outside its regulatory scope. The payment method itself acts as a behavioural guardrail: you can only deposit what you have.

For operators, the shift to PayID brought its own adjustments. PayID deposits are irrevocable — unlike credit card chargebacks, which cost operators time and money to dispute, a confirmed PayID payment cannot be reversed. This eliminates chargeback fraud, which was a significant cost centre for operators accepting credit cards. Some operators passed that savings forward through faster withdrawal processing for PayID users, though this varies by platform.

The ban also accelerated a broader trend that was already underway. PayID’s share of all payments in Australia had been growing steadily, and the gambling ban removed one of the last major use cases where credit cards held an advantage — the ability to deposit on borrowed funds. With that advantage eliminated by regulation, the remaining comparison between PayID and debit cards favours PayID on speed and simplicity.

The legal framework around PayID casinos provides additional context on how the credit card ban fits within Australia’s broader gambling regulation, including the Interactive Gambling Act and ACMA’s enforcement activities.

Looking ahead, the credit card ban is part of a larger regulatory trajectory. The April 2026 advertising reform package — banning gambling ads during live sport broadcasts, at sporting venues, and on player uniforms from 1 January 2027 — suggests the government views payment restrictions and advertising restrictions as complementary tools. If this pattern continues, PayID’s position as the primary deposit method for Australian online gambling is likely to strengthen further, because it is the method most aligned with the regulatory direction: traceable, limited to available funds, and integrated with the banking system’s own monitoring capabilities.